Is Microsoft blocking OpenAI from succeeding in the Enterprise?

OpenAI's Enterprise Problem Isn't the Model, Harness, or App problem. It's a Distribution one.

OpenAI may have kicked off the AI revolution, but there’s a distribution problem brewing that nobody’s really talking about. And it traces all the way back to a deal they signed with Microsoft in 2019.

When Microsoft made its initial investment in OpenAI, the deal came with strings. Big ones. OpenAI’s models would be hosted exclusively on Azure. API access? Azure. Enterprise workloads? Azure. For years, that was fine. Microsoft poured in billions, OpenAI got the compute it needed, and Azure got to be the front door to the hottest AI on the planet.

But the landscape has shifted dramatically since then. And the constraints baked into that original partnership are starting to look less like guardrails and more like handcuffs.

The Multi-Cloud Reality

Here’s what the enterprise AI market looks like right now.

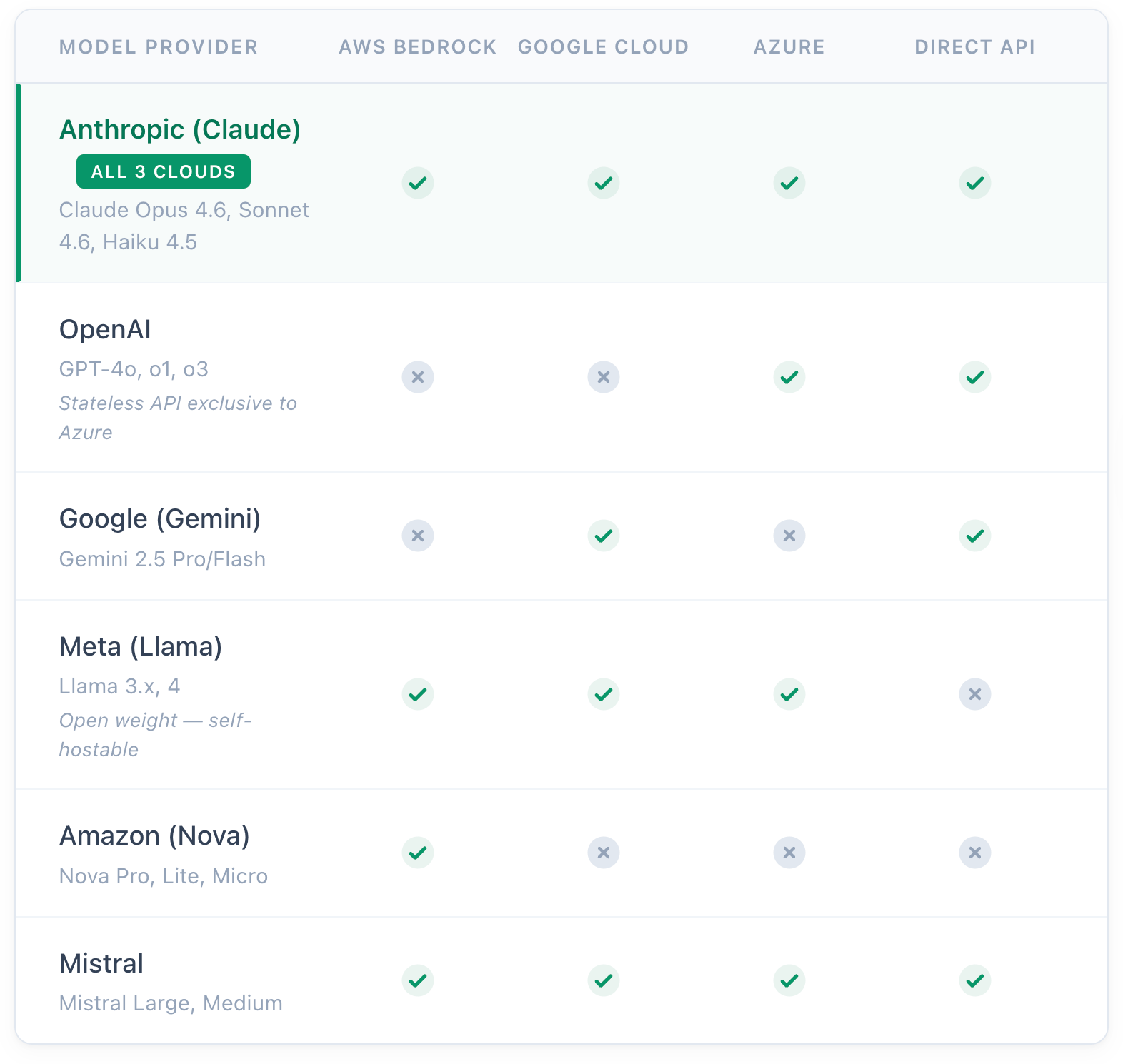

Microsoft Azure can host just about any model. They’ve got OpenAI’s models, obviously. But they’ve also brought in Anthropic’s Claude through Azure AI Foundry. GitHub Copilot, which is part of Azure Foundry, has become one of the most widely deployed developer tools in the enterprise. They’re hedging.

Google Cloud hosts Gemini natively, of course. But they also host Claude models through Vertex AI. Their platform is model-agnostic in practice, and developers and enterprises can mix and match.

Amazon Web Services has Bedrock, which hosts a whole ecosystem: Anthropic’s full Claude lineup, Amazon’s own Nova models, Meta’s Llama, Mistral, and more. It’s a buffet.

And then there’s Anthropic. Claude is now the only frontier AI model available across all three of the major cloud platforms: AWS Bedrock, Google Vertex AI, and Microsoft Azure Foundry. That’s not an accident. That’s a strategy. And it’s working.

The Enterprise Salesforce Advantage Nobody’s Talking About

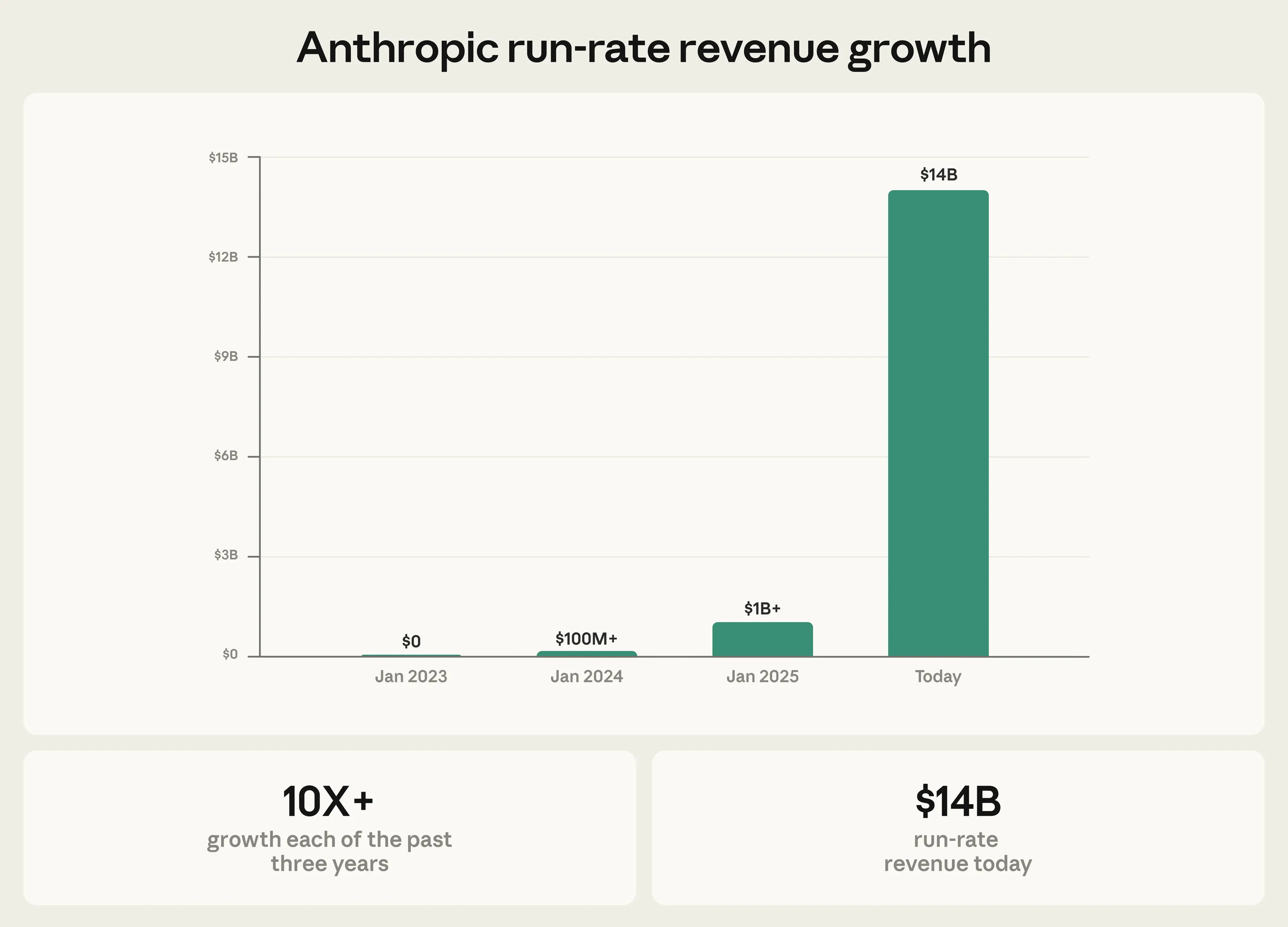

Now, not to take anything away from Anthropic, because they’ve done a phenomenal job with their models. Claude Code has basically taken over every developer’s mind. It’s the most-used AI coding agent on the market, with roughly 46% of developers naming it their “most loved” tool in a recent survey of 15,000 engineers. Anthropic’s run-rate revenue has surpassed $30 billion, up from about $9 billion at the end of 2025.

But here’s the part that I think gets underappreciated: distribution through cloud seller networks.

Amazon, Microsoft, and Google each have tens of thousands of enterprise sellers. Account executives, solution architects, and partner teams, all of them incentivized to sell whatever runs on their platform. And since Claude is available on every major cloud, those sellers can position Anthropic’s models regardless of which hyperscaler their customer is on.

OpenAI doesn’t have that luxury. Their models can’t run on Google Cloud or Amazon in the traditional sense. Their API is exclusive to Azure. So the only enterprise sales force pushing OpenAI models at scale is Microsoft’s. And even Microsoft is now somewhat agnostic, having started offering Claude inside Office 365 and hiring Mustafa Suleyman to build their own in-house models.

Think about that for a second. You’ve got tens of thousands of enterprise sellers at three hyperscalers who can get paid on Claude deals. OpenAI? They’ve got Microsoft. That’s it. And even that relationship is getting complicated.

OpenAI’s Push to Break Free

OpenAI clearly sees this problem, which is why they struck the $50 billion deal with Amazon back in February. AWS is now the exclusive third-party cloud distribution provider for OpenAI Frontier, which is their enterprise platform for building, deploying, and managing teams of AI agents. The two companies are co-creating a “Stateful Runtime Environment” that would run on Amazon Bedrock, giving OpenAI models persistent context, memory, and identity within the AWS ecosystem.

This is OpenAI trying to build a harness around their models, something almost like a Claude Code equivalent, so they can get out from under the Azure-only constraint and actually reach enterprise buyers where they already live.

But here’s where it gets messy.

Microsoft believes this deal violates their exclusivity agreement. Their contract states that all stateless API calls to OpenAI models must be hosted on Azure, and Microsoft executives reportedly think the AWS arrangement crosses the line, both in spirit and in letter. People familiar with Microsoft’s position have been quoted saying, essentially, “We know our contract. We will sue them if they breach it.”

The legal argument hinges on a technical distinction: Microsoft’s exclusivity covers stateless API calls. OpenAI and Amazon are building a stateful runtime environment. Is that a legitimate architectural difference, or is it a clever workaround? That’s what lawyers, and potentially courts, will have to figure out.

I’m genuinely curious whether that contract holds up. Because the reality is that OpenAI is at a competitive disadvantage precisely because they can’t activate distribution into enterprise buyers the way Anthropic can. And they don’t have the sales force to do it single-handedly. They just don’t. You can’t go up against the combined weight of AWS, Google Cloud, and Azure seller networks with a direct sales team, no matter how good your product is.

The Why Cheaper Models Wasn’t The Right Strategy

I’ll be honest. I thought OpenAI’s play with smaller models was going to be the winning move. The nano, mini, small model strategy seemed smart because it’s been difficult to compete on price and performance at that level. OpenAI’s smaller models have had phenomenal intelligence relative to token price. And Anthropic always had Haiku, but it felt like the smaller models were where the real leverage was.

I was wrong. It’s been the race toward the frontier, the most capable and most intelligent models, that’s captured everyone’s attention and, more importantly, enterprise wallets. Opus 4.6, Sonnet 4.5: these models are what’s driving adoption. Anthropic got that right.

Now, I don’t think smaller models and frontier models are contradictory. There’s absolutely a place for small language models. When you’re talking about inline use cases like observability, telemetry, and email classification, things built on something like TinyBERT or other SLMs that need to run on CPUs locally, process quickly, and handle narrow data types, you don’t need a large language model. Fine-tuned SLMs are perfectly suited for that.

But for the enterprise buying decisions, for the platform bets, for the “which AI partner are we going all-in on” conversations happening in boardrooms right now? It’s the frontier models winning those deals. And Anthropic positioned themselves perfectly for it.

What Happens Next

So here’s the question: does OpenAI swing back?

If the Frontier platform on AWS actually launches and works, if they can build this stateful environment that gives enterprises the agentic AI capabilities they want, running natively in AWS, that changes the distribution math significantly. Suddenly OpenAI isn’t just a Microsoft story. They’re accessible through the world’s largest cloud provider, with Amazon’s massive enterprise seller network behind them.

And if they eventually expand to Google Cloud too? That would close the distribution gap entirely.

But that’s a big “if.” Microsoft isn’t going to let this go quietly. The contract dispute is real. The three companies are reportedly in talks to resolve it before Frontier goes live, but if those talks fail, we could be looking at litigation that reshapes how AI-cloud exclusivity agreements are written for years to come.

Meanwhile, Anthropic just keeps executing. They announced a partnership with Google and Broadcom to secure multiple gigawatts of next-generation TPU capacity starting in 2027. They’ve got over 1,000 enterprise customers each spending more than $1 million annually, double what they had just two months ago. Claude Code is authoring roughly 4% of all commits on GitHub. The flywheel is spinning.

The irony is that the deal that once gave OpenAI its biggest advantage, Microsoft’s compute and capital, may now be the thing holding them back from competing in the enterprise market that matters most. Distribution wins markets. And right now, Anthropic has it. OpenAI is fighting for it.

It’s going to be a fascinating year.